austin

2026-06-05

CVX vs. ENB: Two Energy Dividends, Two Very Different Bets

Oil has climbed sharply since early 2026 on sustained geopolitical pressure. Chevron and Enbridge both show up in energy income portfolios. But they make money in completely different ways, and the current environment has made that distinction worth understanding clearly.

What Drove Oil Higher

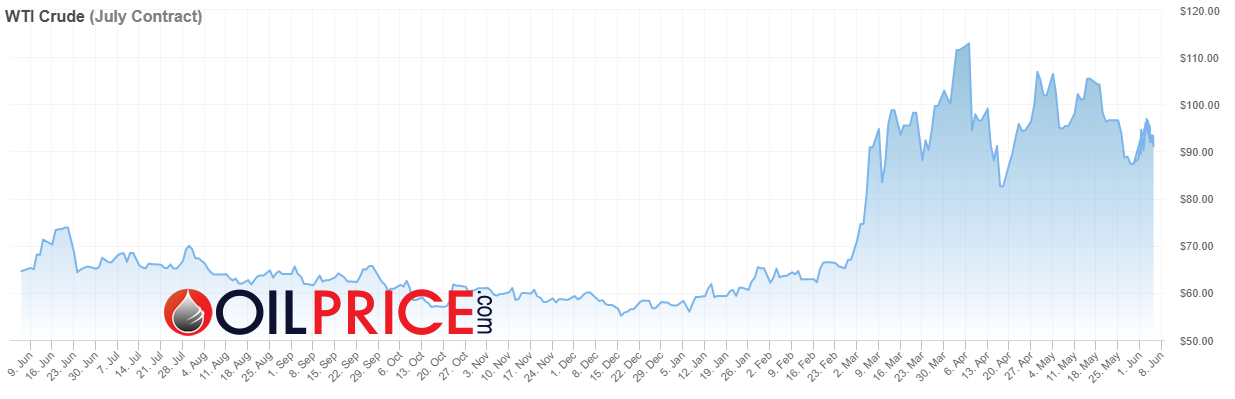

WTI crude began a sustained climb in late February and through March 2026, driven by escalating tensions around the Strait of Hormuz and broader Middle East instability. It peaked around $115 in April before pulling back to the current range of $95 to $96. That is a significant repricing over a relatively short period, and it has made energy one of the more discussed sectors in income investing circles.

Investors holding Chevron or Exxon through that move have done well. Their positions are up, the macro backdrop looks favorable, and the dividend coverage has improved with margins. The question worth asking before adding more energy exposure is what you are actually buying when you buy an energy dividend.

CVX Is an Oil Price Position

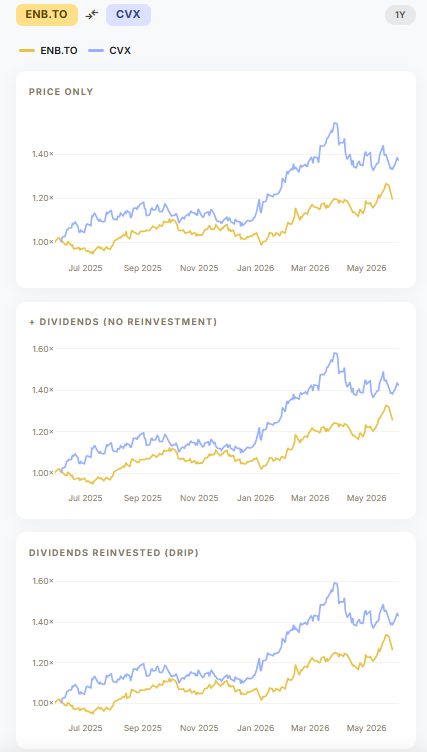

Chevron's income story is tied directly to commodity prices. High oil prices mean high upstream margins. At $96 WTI, free cash flow is strong and the dividend is well covered. If oil pushes to $120, CVX shareholders benefit materially. That leverage is real and it is the reason CVX has outperformed ENB.TO on total return over the past year across all three measures — price only, plus dividends, and with dividends reinvested.

The risk runs in both directions. Oil prices are volatile. A ceasefire announcement, a shift in OPEC production, or a demand shock can reverse a geopolitical premium quickly. During the 2014 to 2016 oil price collapse, Chevron froze dividend growth for several years while burning through reserves to sustain the payout. The dividend survived. But investors who bought at elevated oil prices sat through a materially impaired position for two years before conditions improved.

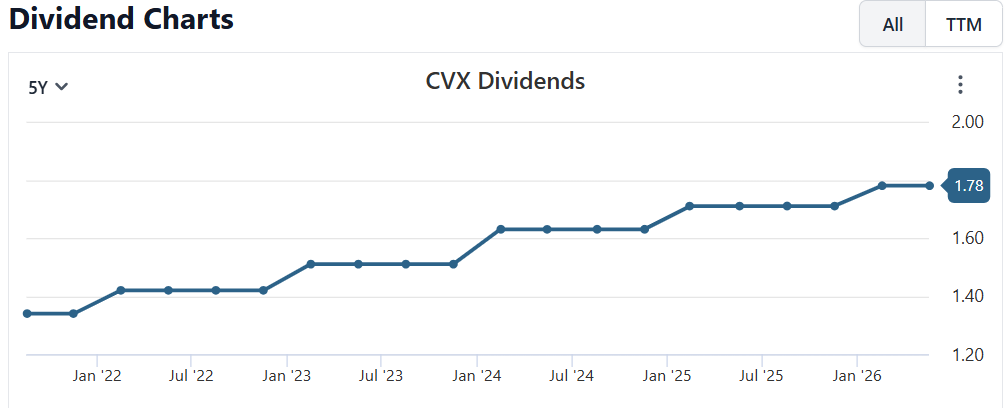

CVX's dividend has grown consistently from roughly $1.42 per quarter in early 2021 to $1.78 today. That is a strong track record. It was built through careful balance sheet management during both high and low commodity price environments. It is not immune to what oil does next.

ENB Is an Oil Flow Position

Enbridge does not sell oil. It moves oil and natural gas through pipes and collects a regulated, contracted fee per unit of volume. Approximately 98% of Enbridge's earnings come from cost of service or take or pay arrangements. The fee gets paid whether oil is at $50 or $96. That is the business model, not a coincidence.

The trade-off is visible in the same chart. ENB.TO did not surge when oil climbed. It has appreciated steadily but has meaningfully underperformed CVX on total return over the past year. Enbridge shareholders gave up the upside of high commodity prices. What they received in return is an income stream that does not depend on where WTI closes on any given day.

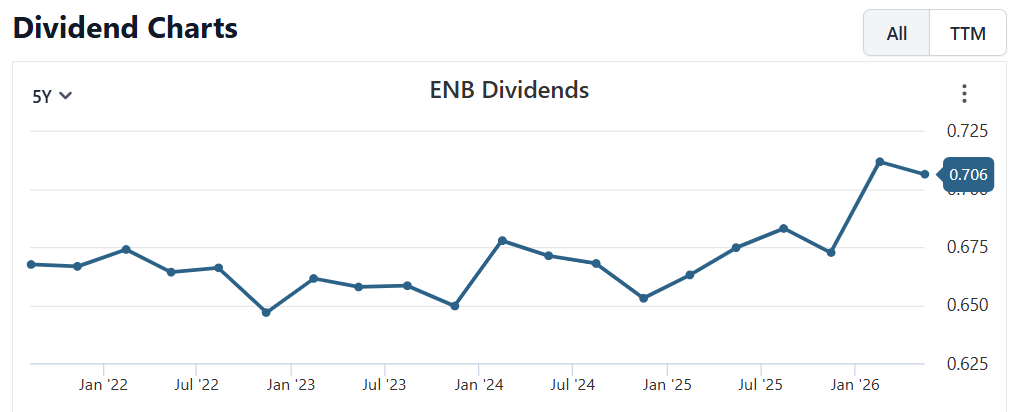

Enbridge's quarterly dividend has grown from roughly $0.67 to $0.706 over the past five years. That growth is modest and the path has not been perfectly smooth. It is more accurately described as stable with slow growth rather than the consistent compounding story that CVX or XOM tell. The honest case for ENB is not dividend growth. It is dividend durability regardless of the commodity cycle.

There is one structural tailwind worth noting separately. Enbridge transports natural gas as well as crude oil. Natural gas demand tied to US data center construction has been running at record levels. AI infrastructure requires consistent fuel supply that has nothing to do with geopolitical events in the Middle East. ENB's natural gas pipeline volumes are benefiting from that demand trend independently of everything happening in the Hormuz region.

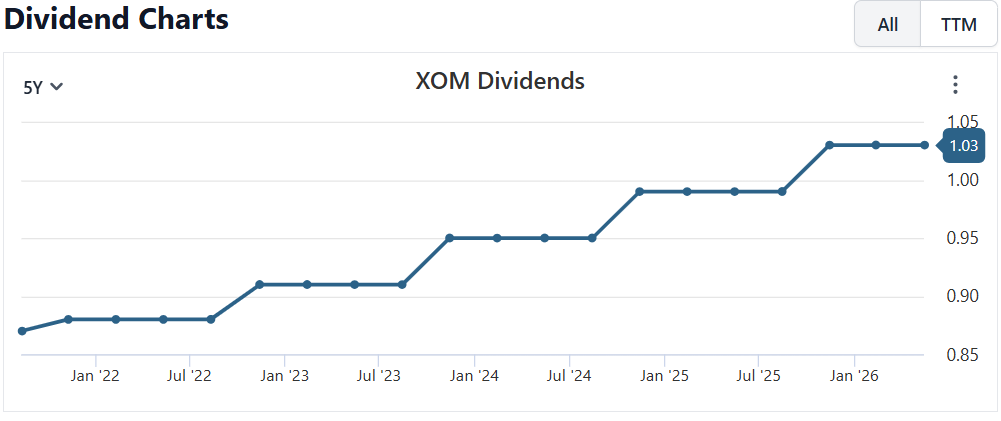

XOM: A Third Data Point

Exxon sits in the same producer category as Chevron. Its dividend has grown from roughly $0.88 per quarter in 2021 to $1.03 today. The growth trajectory is consistent and the balance sheet has been strengthened through the high margin environment of the past few years. Like CVX, the dividend coverage looks strong at current oil prices and weakens materially if oil falls back toward $65 to $70.

What the Honest Trade-Off Looks Like

If oil stays elevated or moves higher, CVX and XOM win on total return. The upstream leverage that creates dividend risk in down cycles also creates the strongest capital appreciation in up cycles. That is a real advantage and the past year's returns demonstrate it clearly.

ENB carries its own risks. Canadian pipeline regulation can change. The long term energy transition creates genuine questions about volume over decades. And the stock will not give you the narrative upside when oil headlines dominate and everyone is discussing $120 scenarios.

The useful distinction is not which company is better. It is what you need your energy position to do. CVX and XOM give you oil price exposure that happens to pay a growing dividend. ENB gives you infrastructure income with volume exposure and almost no commodity price exposure. In an environment where oil can move 30% in a few months and reverse just as fast on a peace headline, those are genuinely different positions in a portfolio.

Holding both is not a contradiction. Knowing which one you own for which reason is the point.

This post is for informational purposes only and does not constitute financial advice. Dividend figures sourced from company investor relations pages and Yahoo Finance as at June 2026. Verify current data before making investment decisions.