austin

2026-05-12

The Quiet Performer: Why Canadian Industrial REITs Deserve a Second Look

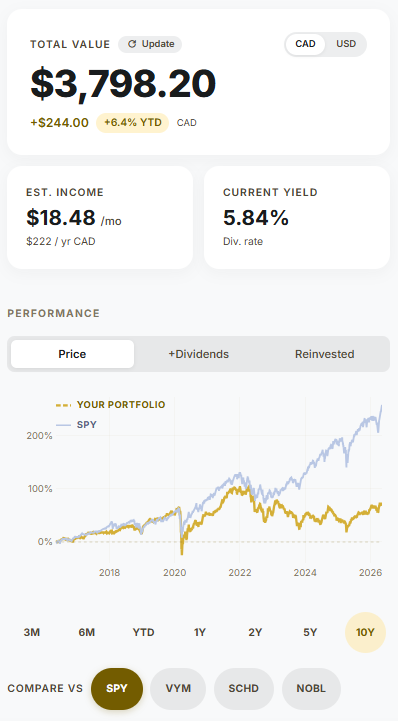

Canadian industrial REITs closely tracked the S&P 500 through the digital transformation boom during COVID, and then got left behind when mega-cap tech drove the recovery. That gap isn't a sign of weakness. For income investors with a 5-year view, it may be the opportunity.

The Chart That Tells the Story

Look at a portfolio of Canadian industrial REITs comprising approximately equal weights of Granite REIT (GRT), Dream Industrial (DIR), ProREIT (PRV), and Nexus REIT (NXR) against SPY over the past ten years. Through 2021, the tracking is remarkably close. Both rode the same macro tailwind: low rates, rising asset values, and a digital economy expanding at pace. Then 2022 arrived, rates rose sharply, and the two lines separated.

SPY recovered through 2023–2025 on the back of a handful of mega-cap tech names. However, industrial REITs didn't follow. Not because their fundamentals deteriorated, but because that rally was narrow, sector-specific, and had nothing to do with logistics, warehousing, or industrial real estate. The price gap you see today reflects a perception problem, not a business problem.

Why the Rate Sensitivity Argument May be Overstated For Some REITs

Rate sensitivity punished the entire REIT sector in 2022, and much of that punishment was deserved. Heavily indebted REITs faced genuine refinancing risk in a sustained high-rate environment, while potentially eroding investors' return through consistent (A)FFO growth and payout through distributions. Investors broadly sold the category, and industrial REITs got caught in the same selloff.

But not all REITs carry the same debt load. The larger industrial names tell a different story:

| REIT | Debt-to-EBITDA | Distribution Yield | (A)FFO Payout Ratio | P/(A)FFO |

|---|---|---|---|---|

| Granite REIT (GRT) | 6.8x | 3.85% | 63% | ~16x |

| Dream Industrial (DIR) | 7.3x | 4.91% | 66.8% | ~13.6x |

| Pro REIT (PRV) | 8.9x | 6.94% | 94.5% | ~13.6x |

| Nexus Industrial REIT (NXR) | 10.5x | 7.94% | 99.1% | ~12.5x |

GRT and DIR carry meaningfully lower debt relative to earnings than the broader REIT sector, with payout ratios leaving genuine cushion for distribution sustainability. The rate sensitivity argument that correctly identified risk in overleveraged REITs applies with considerably less force to these two names. You don't need a view on where rates go next to own them. Rather, you need a view on whether industrial real estate demand holds up.

PRV and NXR tell a slightly different story. The higher yields are real, but the high payout ratios leave almost no margin for error. Any meaningful softness in occupancy or rent growth puts those distributions at risk. The market is already pricing some of this in: NXR trades at the lowest P/AFFO multiple in the group at 12.5x, reflecting the higher leverage and payout risk. These are not set-and-forget income positions. They reward investors who follow the underlying fundamentals closely and size the position accordingly.

Digital Transformation Built This Thesis. AI Extends It.

The demand story behind industrial REITs is straightforward. E-commerce growth through COVID drove an unprecedented need for logistics space, fulfillment centres, distribution hubs, cold storage. Industrial vacancy rates fell to historic lows. Rents rose. The REITs that owned this space collected the benefit.

AI doesn't reset that thesis; I believe that it cab extend it as it further accelerates the digital transformation. Faster digital adoption means more logistics complexity, more onshoring of supply chains, more demand for the physical infrastructure that moves and stores goods. The digitization wave that COVID accelerated is not reversing; AI makes it structural. Industrial real estate sits at the intersection of every supply chain that needs to move faster and more intelligently.

Why Generic REIT ETFs Don't Give You This Exposure

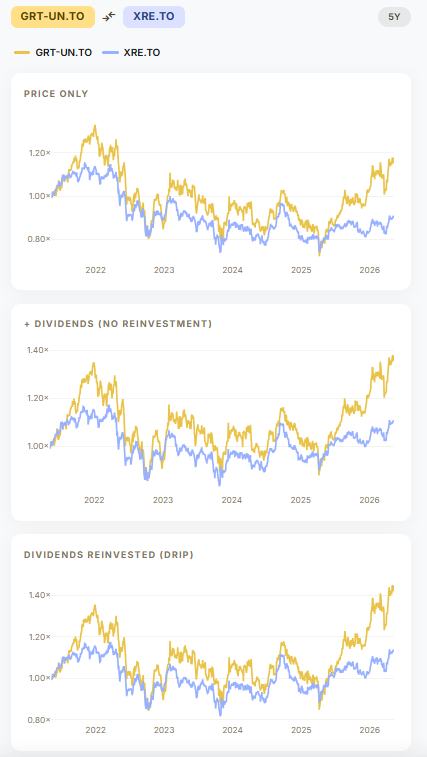

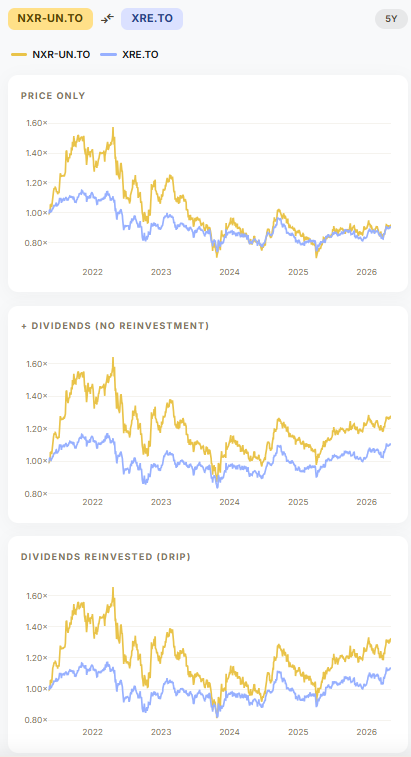

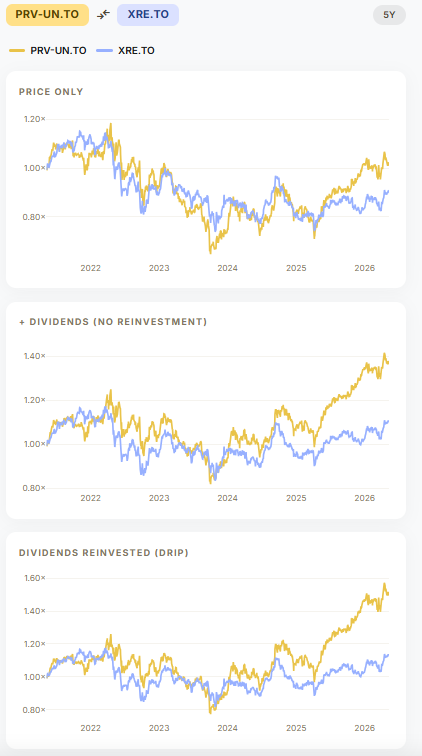

The instinct to buy a Canadian REIT ETF like XRE for diversified real estate exposure is understandable. The problem is composition. Generic Canadian REIT ETFs carry substantive amount of other REITs in residential, retail, office sector, reducing overall industrial exposure. A holder of XRE who believes in the industrial demand thesis is largely not getting the upside.

Each of these four names has outperformed XRE on a 5-year total return basis. The ETF provides diversification; it also dilutes the specific exposure you're trying to own.

Big vs. Small: Two Ways to Own the Theme

GRT and DIR can be the core allocation as these names carry larger balance sheets, lower leverage, and payout ratios, which leave room for distributions to hold up even if conditions soften. GRT's 63% AFFO payout and DIR's 66.8% FFO payout mean both funds have genuine cushion. The trade-off is relatively lower current yield: 3.85% and 4.91% respectively. For income investors who want the industrial thesis without distribution risk, these are the straightforward entry points.

PRV and NXR may require different risk profile. The yields are enticing at 6.94% and 7.94%, while holding genuine industrial exposure to the same demand tailwinds. But high debt-to-EBITDA and high AFFO payout ratios can mean that the distribution will only hold as long as everything going right: stable occupancy, rent growth holding, no significant refinancing surprises. These are positions that reward active monitoring, not passive holding. Unless you can stomach and monitor these risks, size them as satellite positions, not your core positions.

Together, the four names offer a tiered framework to own REITs with industrial exposure. One may consider to own large, safe names like GRT and DIR for reliable, relatively stable picks, while adding PRV and/or NXR in proportion to your conviction and risk tolerance, while boosting overall distribution yield of your portfolio.

The Entry Case Today

You don't need to predict interest rates to make this investment. You need to believe two things: that digital infrastructure demand, such as logistics, fulfillment, industrial space continues to grow over the next five years, and that the current price gap versus broad equity markets reflects a sentiment overhang rather than a fundamental deterioration.

The financial metrics of GRT and DIR suggest the fundamentals can hold well through the rate cycle. The price hasn't caught up yet. For an income investor collecting stable distributions while waiting for that gap to close, that's a reasonable place to be positioned. If you have real conviction over high growth and resilience in the sector and can stomach the risk, you may want to take a flyer at some of the small industrial REITs like PRV or NXR for that juicy yield. I'll let you decide what works for your own investment.

This post is for informational purposes only and does not constitute financial advice. Always do your own research before making investment decisions.