austin

2026-06-22

Your "Diversified" Index Fund Is More Concentrated Than You Think

Same 500 Stocks, Very Different Outcomes

The cleanest way to isolate this is to compare SPY against RSP, the equal weight version of the same S&P 500. Same 500 companies. Same starting universe. The only difference is the weighting method. SPY lets winners grow into larger and larger positions. RSP resets every holding back to roughly the same weight at each rebalance.

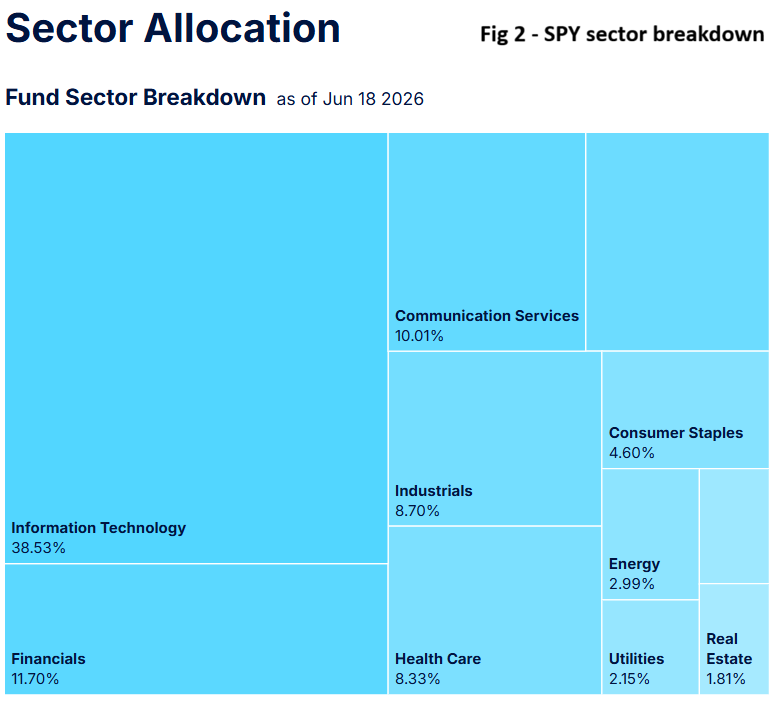

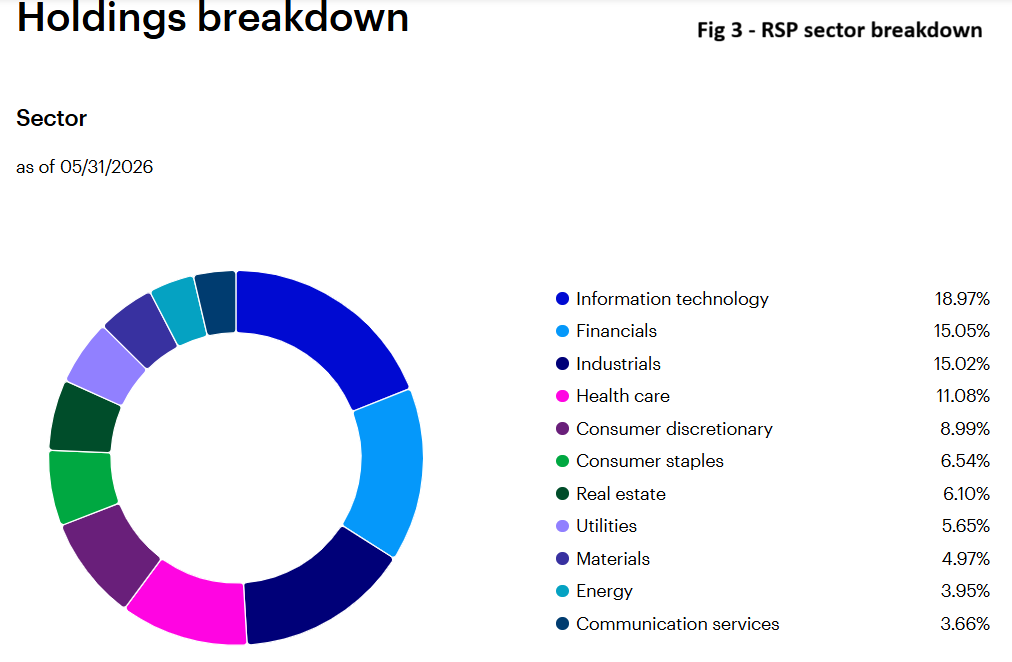

The sector breakdowns make the mechanism visible. As of late May 2026, RSP's largest sector is information technology at 18.97%, followed closely by financials at 15.05% and industrials at 15.02%. No single sector dominates. SPY, holding the same 500 companies, carries 38.53% in information technology alone as of mid June 2026, more than double RSP's weight in the same sector. Financials, the second largest sector in SPY, sits at 11.70%, lower than RSP's weight in the same category.

This is the concentration argument with numbers attached. Both funds own the same 500 companies. One of them has put nearly 39 cents of every dollar into a single sector. The other has spread its largest sector exposure to under 19 cents. That is not a difference in what you own. It is entirely a difference in how much of each thing you own.

Here is the part that needs to be said plainly. Over the past five years, SPY returned roughly 75% on price alone. RSP returned roughly 40%. That is not a small gap. The concentration that equal weighting is designed to avoid has been exactly the right bet for half a decade. The companies driving SPY's return were not a fluke. They were the market, and a 38.53% weight in information technology is the reason.

This matters because it changes what the argument for equal weighting actually is. It is not a performance pitch. The data does not support that. It is a concentration risk argument. RSP gives you genuine diversification across company size and sector. What it has cost you, at least for the past five years, is real return. Anyone telling you equal weight is simply the smarter way to hold the S&P 500 is leaving out the chart above.

Why the Gap Exists

The mechanism is straightforward. When a handful of companies grow faster than the rest of the index, a cap weighted fund lets them compound into larger positions. An equal weight fund rebalances that growth away, selling some of the winner and redistributing into the rest of the index. If the winners keep winning, that rebalancing is a drag. If the winners eventually mean revert, or if leadership broadens to smaller names, the same mechanism becomes a tailwind.

The honest takeaway is that this is a bet on market regime, not a free upgrade. Equal weight has historically done better in periods when market leadership is broad and mega caps are not running away from everything else. It has done worse, clearly, in a period dominated by a small number of very large winners. The past five years were the second kind of period.

The Canadian Angle: A Different Kind of Concentration

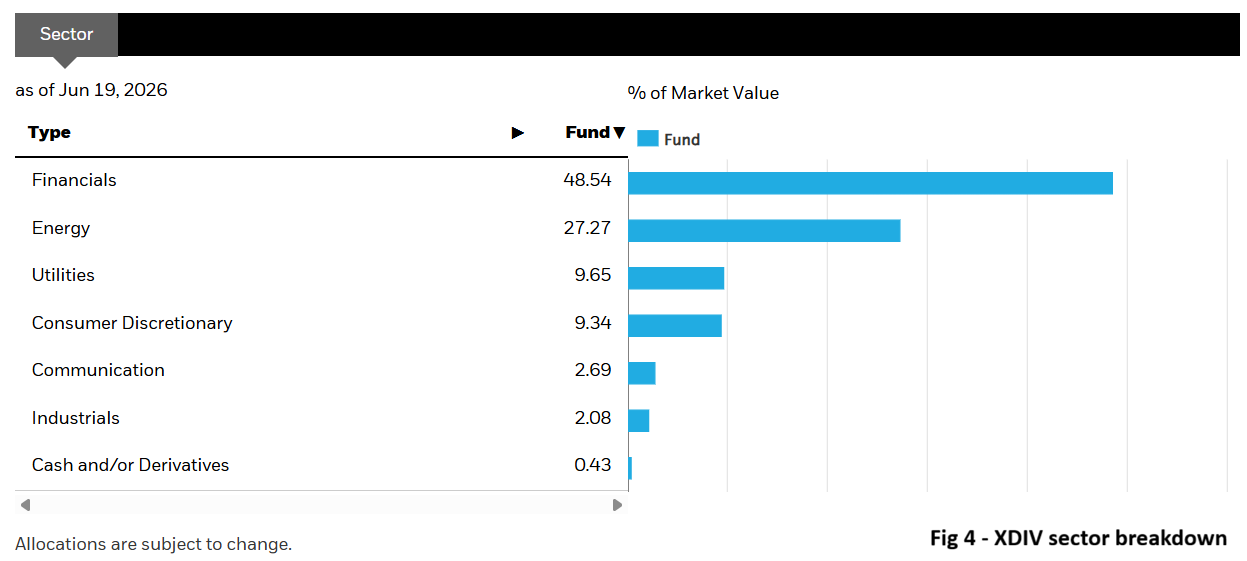

Concentration risk is not unique to the S&P 500. Canadian dividend funds like XDIV carry their own version, and the numbers are more extreme than anything in the SPY versus RSP comparison above. As of mid June 2026, XDIV holds 48.54% in financials and 27.27% in energy. Combined, those two sectors account for nearly 76% of the fund. Utilities and consumer discretionary make up most of the remainder, at 9.65% and 9.34% respectively. Industrials and communication services barely register, at 2.08% and 2.69%.

Put plainly, XDIV's single largest sector weight, financials at 48.54%, is higher than SPY's largest sector weight of 38.53% in technology. A fund marketed as a diversified Canadian dividend holding is, by this measure, more concentrated than the cap weighted US index fund this entire post has been critiquing. And the concentration in XDIV is not split across many names within financials and energy the way SPY's tech weight is split across dozens of companies. Canadian financials and energy are dominated by a small handful of banks and producers, which means the actual single name exposure inside that 76% is significant.

This is the same structural pattern you see when comparing European indices to the S&P 500. European benchmarks skew toward financials, industrials, and energy, and have lagged the US market for most of the past decade precisely because they have so little exposure to the mega cap tech names driving US returns. A Canadian dividend investor buying XDIV is making a similar bet, intentionally or not. You are diversifying away from US tech concentration. You are doing it by concentrating into financials and energy instead, and doing so more heavily than the fund you were trying to diversify away from.

Neither choice is wrong. But "diversified" is doing a lot of work in both cases, and it is worth being precise about what kind of concentration you are trading for what kind.

What to Actually Check

Before assuming any fund gives you broad, even exposure, look at two numbers. The first is the weight of the top 10 holdings. The second is the weight of the largest sector. A fund can pass the first test and fail the second, the way XDIV does. A fund can pass both and still have concentrated all its risk in a single weighting methodology's recent winners, the way SPY has for the past five years.

RSP is not a better version of SPY. XDIV is not a flawed version of a dividend fund. They are different bets on what kind of concentration you are willing to hold. The label on the ticker will not tell you which one you are actually carrying.

This post is for informational purposes only and does not constitute financial advice. RSP vs SPY performance data through June 17, 2026. Sector weightings sourced directly from fund provider websites: RSP as of May 31, 2026, SPY as of June 18, 2026, XDIV as of June 19, 2026. Sector composition shifts over time and figures should be reconfirmed before relying on them for current decisions.