austin

2026-05-25

That 12% Yield Isn't Paying You What You Think

What the Headline Number Leaves Out

Covered call ETFs generate income by selling call options on their underlying holdings. Those calls cap how much the ETF can gain when the market rallies. In exchange, you collect premiums. Those premiums get paid out as your monthly distribution.

That sounds straightforward. Here is where it gets complicated.

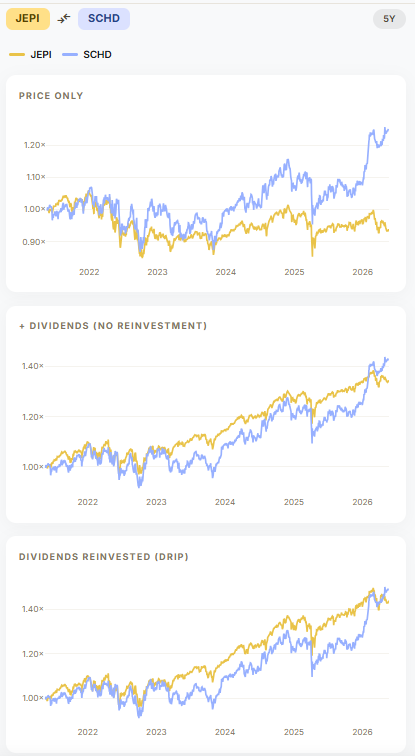

When the S&P 500 runs 20% in a year, JEPI might capture 10 to 12% of that move before handing you your premium check. The gap between what the market returned and what you received does not show up in the yield figure. It shows up quietly in your ending balance.

Over the trailing three years, covered call strategies like JEPI have returned roughly 25 to 30% in total. SCHD returned approximately 35 to 40% over the same period. SCHD pays a yield that looks far less impressive on paper. It still came out ahead. Not because SCHD is a special product. Because it was growing your capital instead of distributing it back to you.

Sometimes You Are Just Getting Your Own Money Back

This is the part that trips most people up. When covered call ETFs pay distributions, a portion of that payment can be return of capital. That means the fund is returning your own invested principal to you. It is not income generated by the portfolio.

The fund's NAV drifts sideways or declines slightly over time as a result. In a taxable account, return of capital is not taxed as income when you receive it. It reduces your cost basis instead. But the bigger issue is simpler than tax treatment. Your pile of money is not growing. The monthly checks are real. The wealth creation is not.

To be fair, covered call strategies hold up better than pure equity in choppy or sideways markets. The premium income provides real cushion when prices are not moving. That is a genuine structural benefit. But it depends heavily on the market environment you happen to be investing through.

The Yield on Cost Problem Nobody Talks About

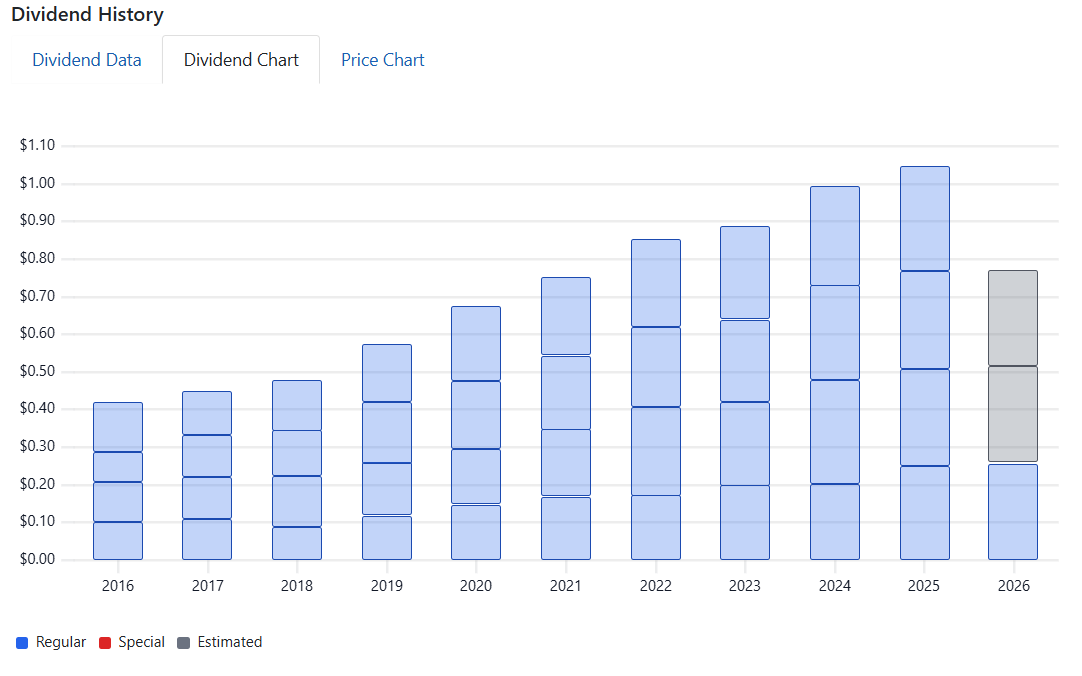

SCHD's current yield of around 3.5% looks boring next to JEPI's 9%. That comparison only makes sense if you are buying today for the first time.

Someone who bought SCHD five years ago has watched the dividend grow from roughly $2.25 per share in 2021 to over $2.80 by 2024. That is a compound annual growth rate of 7 to 10%. Their yield on cost today is closer to 5 to 6%. Meanwhile, covered call distributions move up and down with market volatility. When volatility is low, premiums compress and the distributions shrink. The income stream does not grow. It fluctuates.

Source: chart generated in dividendhistory.org/payout/SCHD/ on May 25, 2026

The 3.5% headline yield is a snapshot of one moment in a growing income stream. Treating it as a fixed number understates what SCHD actually delivers to a long term holder.

Where Covered Call ETFs Actually Make Sense

Covered call ETFs are not a bad product. That is the easy take and it misses the point entirely.

For an investor who genuinely needs income today, covered call strategies make a strong case. Retirees drawing down their portfolios benefit from the regular monthly payments. The reduced volatility profile helps. The cushion in sideways markets is real. These are structural advantages that matter when cash flow is the primary goal.

The mismatch happens when accumulators reach for a 12% yield without needing current income. They trade long term growth for short term distributions they do not actually need yet. The monthly payments feel productive. The total return comparison tells a different story five years later.

Two Questions Worth Answering Before You Buy

Do you need this income now? And have you compared total return against the alternatives, not just the yield?

If you are in accumulation mode, a growing dividend stream like SCHD's compounds in a way that covered call distributions structurally cannot. If you are in distribution mode and drawing down your portfolio, covered call ETFs earn their place. Just understand that the income you receive moves with volatility. It will not be the same number every year.

The yield number on the label tells you what you will collect this month. It says nothing about what your investment will be worth in three years. Those are two different questions. Most investors who end up disappointed by high yield portfolios were only asking the first one.

This post is for informational purposes only and does not constitute financial advice. Performance figures are approximate and based on historical data, which does not guarantee future results.